Live Real Estate News

[wp-rss-aggregator]

St Louis Real Estate News is updated periodically we bring you relevant area news for the St Louis Region

On Tuesday, the Consumer Price Index (CPI) data came in cooler than expected, and the bond market loved it, driving mortgage rates lower. Where do we go from here? Headline inflation is still very elevated historically, but the trend can be our friend over the next 12 months.

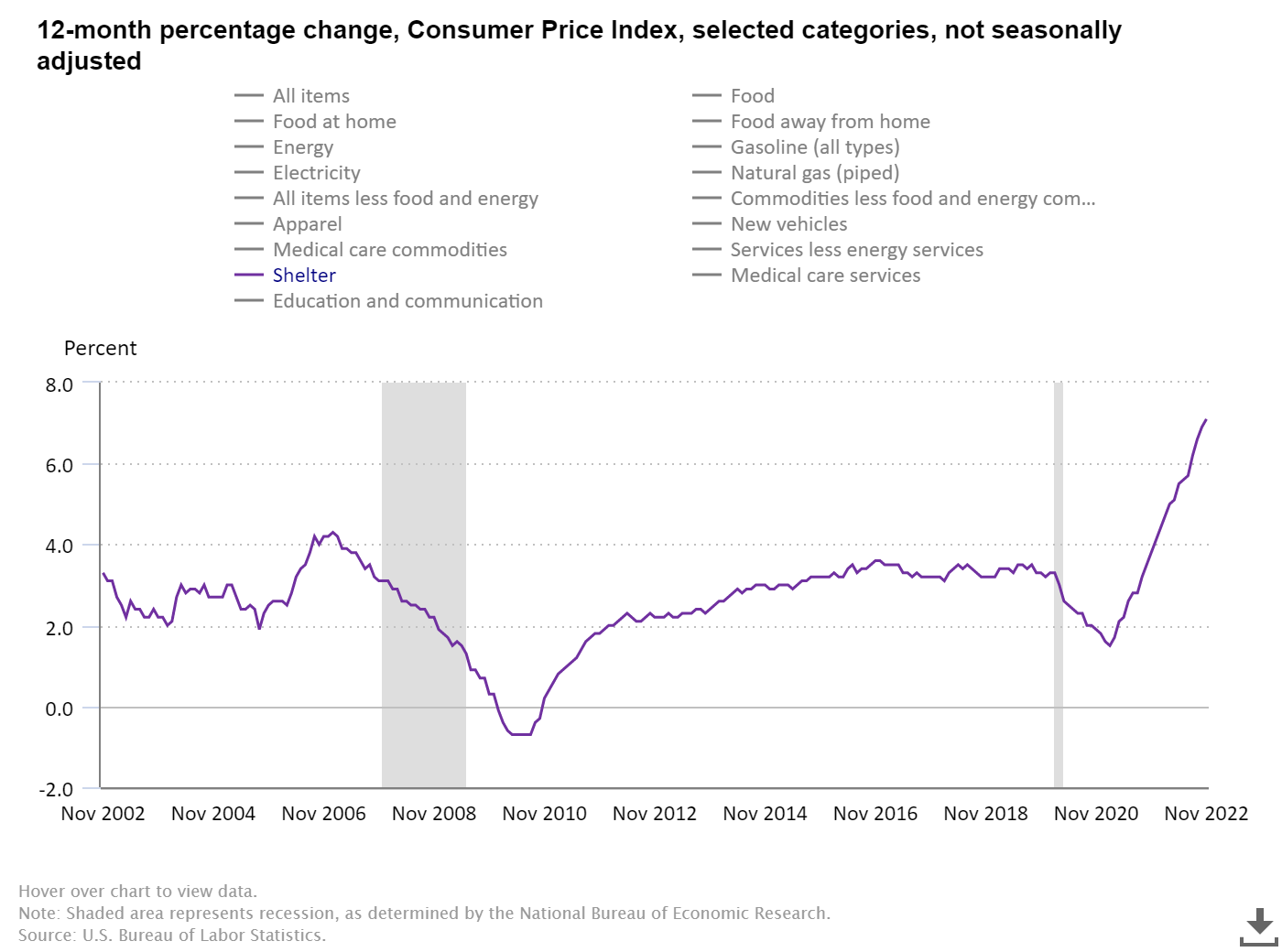

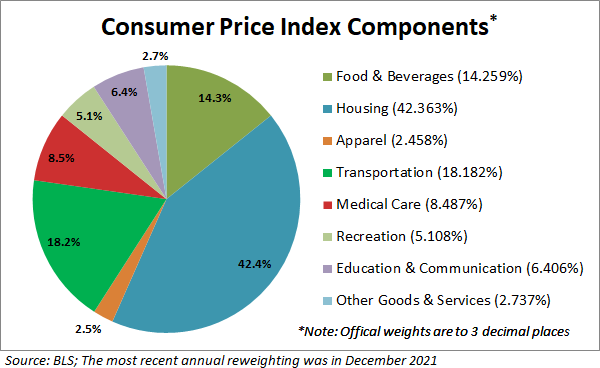

I say this because the most significant component of Core CPI is shelter inflation. The growth rate for rent is already cooling down in real-time data, but the shelter inflation data line of the CPI lags behind the current market reality. This means that what is happening in the present world isn’t showing up in the CPI, which is a big deal since 42.4% of this index is shelter inflation.

As I am writing this, the bond market’s reaction looks like this: the 10-year yield went lower in yields right after the report and is currently trading at 3.48%; this means mortgage rates are going lower today. As the growth rate of inflation fades more and more, the fear of 8%-10% mortgage rates, which was the fantasy of every American bear, is slowly slipping from their fingers because those mortgage rates would be very problematic for the housing market and the economy.

The housing market already went into recession in June of this year, and the second year of every recession is the excruciating part.

Also, the U.S. dollar is heading lower, which is a must because the dollar was getting too intense and creating a lot of havoc worldwide. Traditionally, when the dollar gets too strong, it can cause drama in the financial markets, as it did earlier in the year. The recent cooldown is necessary to create a more stable global market while everyone works on slowing inflation down.

Remember, it wasn’t long ago that the international institutions called for the Federal Reserve to stop its mortgage rate hikes as the dollar created a lot of damage in the markets.

We have had back-to-back reports of more excellent than anticipated inflation data. This is a start, and as I have said over the last few months, we will be in a much different spot 12 months from now.

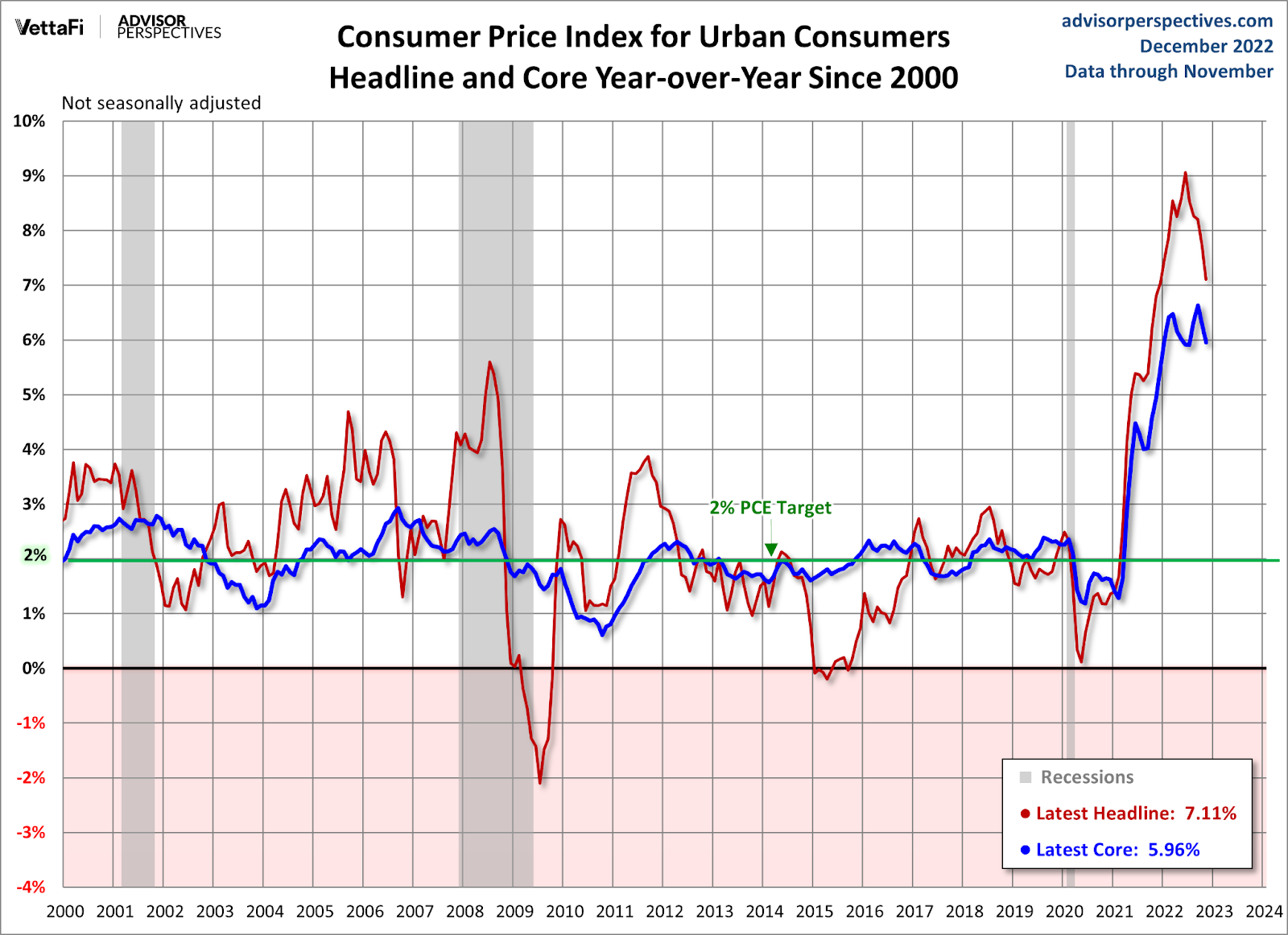

From the BLS: The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.1 percent in November on a seasonally adjusted basis, after increasing 0.4 percent in October, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 7.1 percent before seasonal adjustment. — The all items index increased 7.1 percent for the 12 months ending November; this was the smallest 12- month increase since the period ending December 2021. The all items less food and energy index rose 6.0 percent over the last 12 months. The energy index increased 13.1 percent for the 12 months ending November, and the food index increased 10.6 percent over the last year; all of these increases were smaller than for the period ending October

As you can see below, the month-to-month data is cooling down, and in all honesty, the headline core CPI data is being artificially held up by a lagging indicator. So, the bond market understands this — it has always understood this — which is why the 10-year yield never got to 8%-10% like some people thought it should.

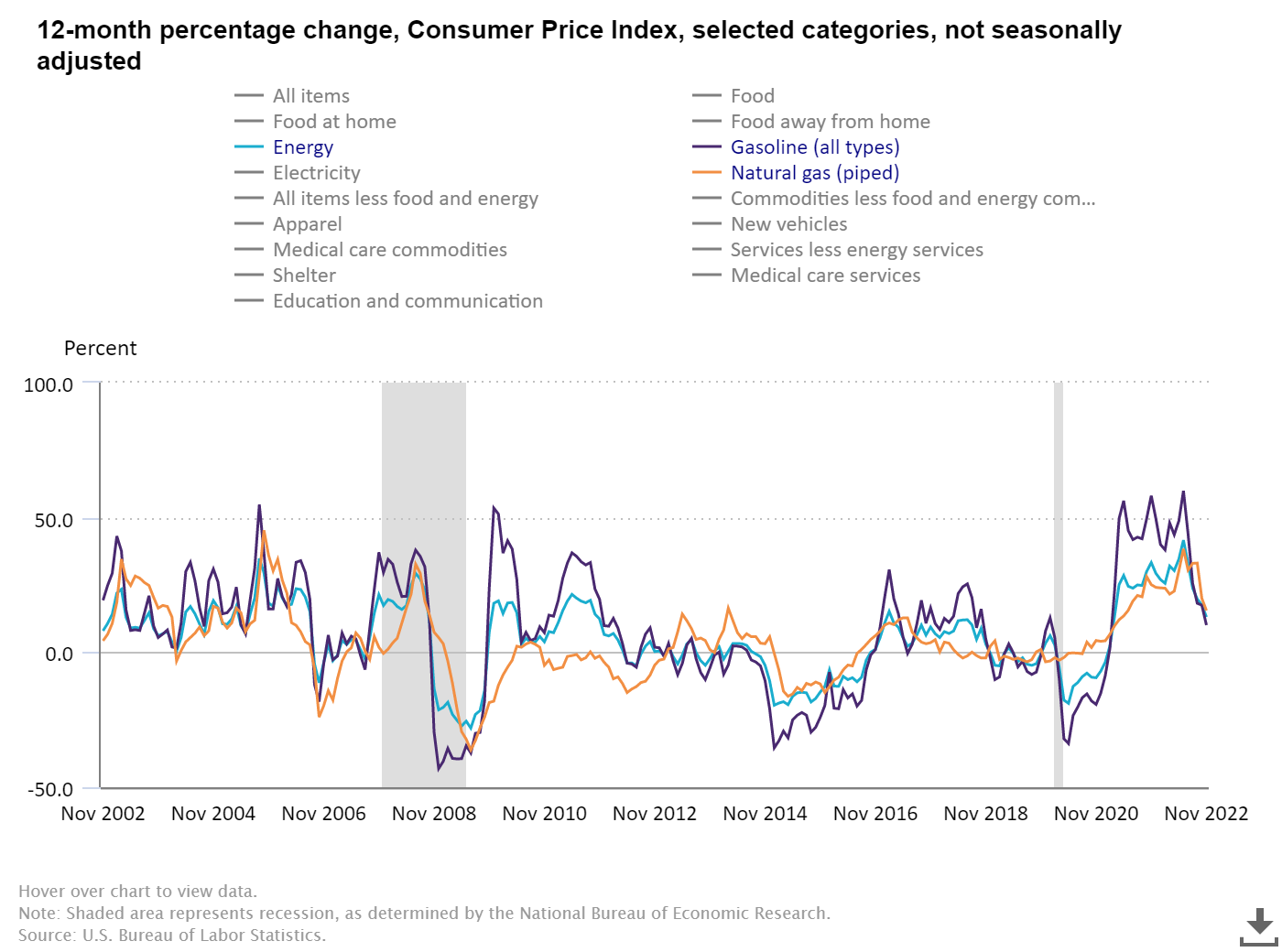

In the Mad Max basket, as I call the energy index, the growth rate is cooling down as oil prices and gas prices have fallen. In March we had the new variable of the Russian invasion of Ukraine, and Russia has used energy as the commodity war of choice against the west, so we aren’t out of the woods on this one as long as that variable is in play. However, for now, oil prices have fallen from their recent peak.

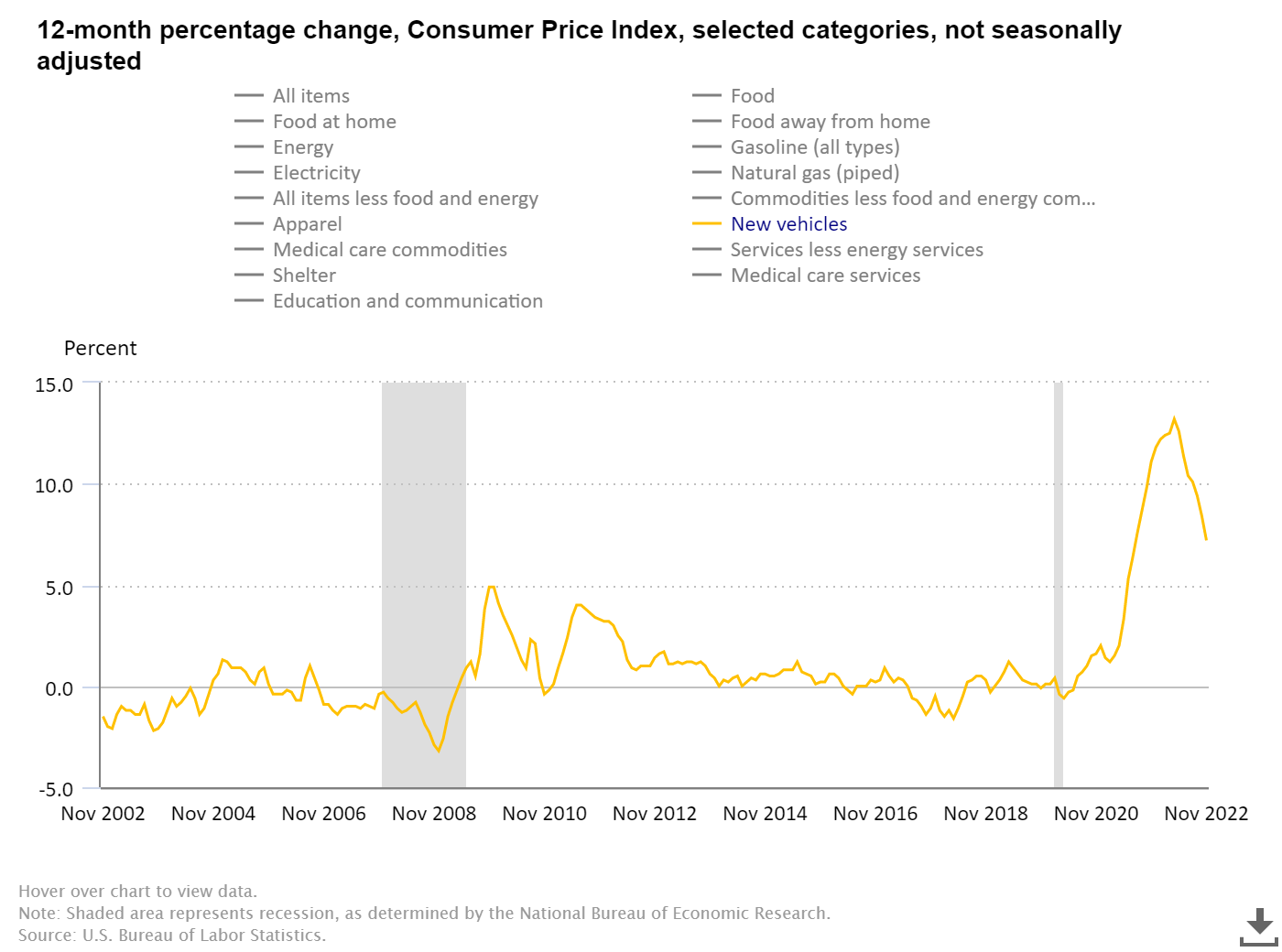

I am glad I bought my new car in October of 2020; car inflation has gone gangbusters, and a lot of this was due to the global pandemic. Auto production slowed immediately during the pandemic, and getting chips and parts to build a car took much longer than normal. However, the inflationary growth rate of the new vehicles portion of the CPI data is falling and has room to go lower.

Food inflation has gone bonkers post COVID-19. Has anyone seen egg prices recently? The growth rate has cooled off a tad. Food inflation is part of headline inflation, not core inflation, and has had historical wild moves. Still, the recent food inflation we have seen has been historically high for the United States.

As you can see, the year-over-year growth rate in inflationary data has peaked for the year. Since we are almost going into 2023, that isn’t saying much.

The following 12 months is what matters, and the best way to fight inflation is always adding more and more supply. If you’re trying to destroy inflation by killing demand by putting Americans into a job-loss recession — that isn’t the best long-term solution, you’re too late on the supply store.

Eventually, you need supply to come back online because people can’t stay unemployed forever. Core CPI inflation is boosted by a data line that is nowhere close to reality. Shelter inflation is not only cooling off; it will compete with the 1 million rental units coming online next year.

As you can see, I am looking out to the future with this because 12 months ago, we didn’t have many mortgage rate hikes in the system, and the growth rate of inflation wasn’t cooling off. Now, it’s a much different story.

We don’t need to create a job-loss recession to bring down inflation; we need more supply. In some parts of the economy, it takes too long to get that supply on, and some are much quicker.

However, with the mortgage rate hikes in place and knowing that the primary data line is lagging, we can hopefully assume that the Federal Reserve, which is a single-mandate Federal Reserve now and all about price stability, will move to a dual-mandate Federal Reserve. The dual mandate Fed is all about price stability and jobs. We need more time to get supply up, and we don’t need to overdo with rate hikes at this stage of the economic cycle.

We are still far from the Fed’s 2% inflationary target, but we don’t need to destroy the economy to get there. Since all six of my recession red flags are up, and I hope the growth rate cools down, mortgage rates can fall, which will stabilize the housing market, which in turn means the U.S. could avoid a recession near term.