Live Real Estate News

[wp-rss-aggregator]

St Louis Real Estate News is updated periodically we bring you relevant area news for the St Louis Region

With home prices accelerating as they are, homeowners today are sitting on a collective $22.7 trillion in equity, the highest amount since analysts began collecting such data in 1945. That is according to a LendingTree study that examines one reason why borrowers hesitate to request home equity loans—they fear their credit will take a hit.

With home prices accelerating as they are, homeowners today are sitting on a collective $22.7 trillion in equity, the highest amount since analysts began collecting such data in 1945. That is according to a LendingTree study that examines one reason why borrowers hesitate to request home equity loans—they fear their credit will take a hit.

“Many homeowners aren’t rushing to tap their equity,” wrote Tendayi Kapfidze, LendingTree’s Chief Economist and VP. “In fact, certain types of home equity borrowing in 2020 hit their lowest level in more than 16 years.”

He says there are multiple reasons for this (including stricter lending guidelines and a fear of over-leveraging).

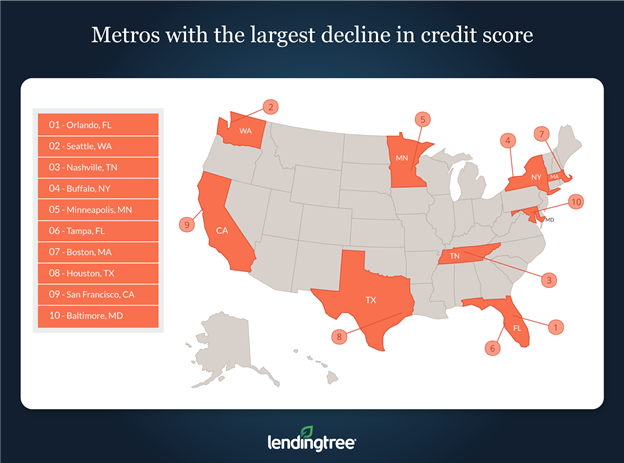

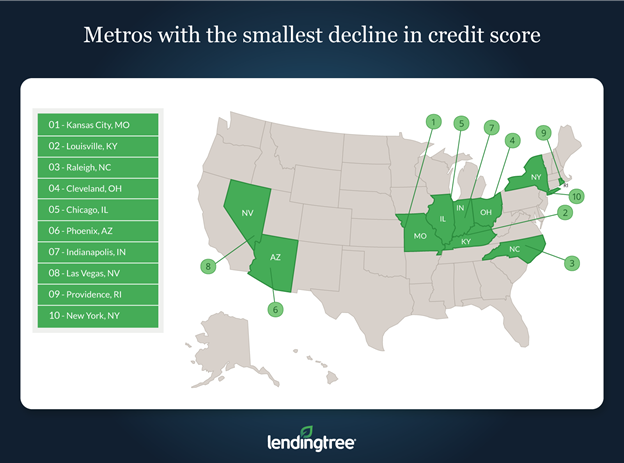

However, he adds, “borrowers need not be afraid that tapping their home equity could hurt their credit scores, at least not in the long term,” a statement he bases on data collected from 1,500 borrowers across 40 metropolitan areas who applied for a second mortgage.

“Although most borrowers do see a decline in their credit score after taking out a home equity loan, the decline tends to be relatively small and their credit score usually recovers in less than a year’s time,” he said.

Here are some of the study’s key findings:

On average, according to the study, scores tended to fully recover to their pre-loan average in less than a year. The complete cycle to return the credit score to its former position before the home equity loan takes an average of about 201 days.

Because a home equity loan likely will negatively impact a borrower’s credit in the short term, Kapfidze offers a few recommendations for homeowners anxious to bounce back from that decline faster.

It is best if borrowers refrain from applying for further credit while recovering from the home-equity loan hit, he said.

“If you continue to apply for new forms of credit right after taking out a home equity loan, then your credit score may not only fall further, but also take longer to rebound,” her said. “As a result, the fewer new credit applications you submit, the better off your score is likely to be.”

He also suggests using as little credit as necessary during this period, paying every bill on time, and looking into debt relief programs should that be a problem.

The full study is available at LendingTree.com.